"This was a lie -- 100 percent lie," Stratton said. "We ran off the guidelines. We met every single qualification to get a HAMP mod."

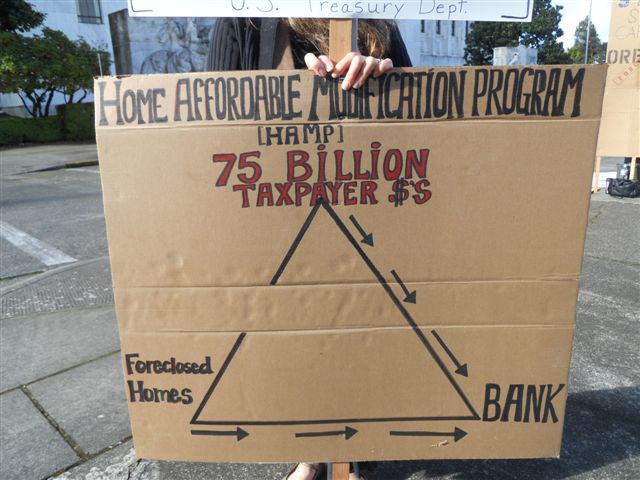

This sign says it all. (courtesy of HuffPost)

The flow of money from the people to the banks is ongoing. This entire real estate crash was orchestrated to move money and assets from the American People to the banks. Not only did the taxpayers our government give the banks and other private companies like GM and Chrysler money to aid and abet them in their journey to control us all through controlling our wealth, but the government participated and is still participating in this scam.

What has this country come to? How have we, the people, allowed this to happen. You will notice there is no major outcry, no major show of disgust. Only a handful of people feel safe enough - or are simply so fed up they don't care about their safety - to protest in public.

We have had and still have unjust wars, wars that have taken thousands of American lives and hurt and disabled hundreds of thousands, yet no public outcry or show of disgust. What has this country come to?

Many of us are old enough to remember the protests by the hundreds and hundreds of thousands against the war in Viet Nam - another unjust war - our government got us into under the guise of national security and for the sake of Democracy. A Democracy we have not seen or enjoyed in this country for quite some time.

The mortgage crisis was made by design. The foreclosure process is by design. The Mortgage Modification programs such as HAMP also by design but designed to fool you into thinking those we elect to office really and truly care about us. Folks, they don't. For our politicians it is all about the money as well. Their lifelong jobs and benefits. Their princely lifestyles. Their travel at our expense on lavish airplanes, staying at the priciest hotels under a shroud of security most Presidents of other countries would like to have.

We are witnessing the final stages of the creation of the "New World Order". Remember, the New World Order President George H.W. Bush talked about. The same one Meyer Rothschilld talked about creating when he said, "Let me control the money of a nation and I care not who makes its' laws". Yes, a plan laid down in the late 1700's coming to full fruition today.

To think all of this is just an economic bubble that occurred by itself, think again. All bubbles are man made. They are made by design with the sole purpose of amassing money by the billions. Bubbles are made to control an economy and most of its wealth by a handful of people whose patriotism and care for their fellow citizen stops at the edge of their bank accounts - most of which are off shore.

Stop and think. Banks all said they were broke or going broke. They needed the infusion of trillions of dollars to stay afloat and if they did not get the money our entire world economy would crash. WRONG! They didn't need the money. They didn't lose any money and they are still not losing any money. No one has ever asked the question, "where did all the money go that they made during the bubble?". They made loans, sold the loans to Wall Street who in turn sold those packaged loans to unwary investors the world over. Where did all that money go that they made? No one knows for sure but I believe they have it all off shore. All The banks have major operations the world over and the money that goes there never gets reported here.

I still have that same question; "Where's The Money?".

Check out this story in the Huffington Post.com

WASHINGTON -- Judy Stratton said she and her husband Harry have tried since January 2009 to modify the mortgage on their home in Stayton, Ore. after a drop-off in demand for Harry's floor maintenance services. In August, Stratton said, they received a rejection letter from their bank saying they did not qualify for help per the Obama administration's Home Affordable Modification Program.Read more...click here

"This was a lie -- 100 percent lie," Stratton said. "We ran off the guidelines. We met every single qualification to get a HAMP mod."

protection racket--the truth

ReplyDeleteU.S. Seeks to Shield Goldman Secrets .

Goldman Sachs Group Inc. has always closely guarded the secrets of its lucrative high-speed trading system. Now the securities firm is getting a help from an unusual source: federal prosecutors.

Federal prosecutors in Manhattan this week asked a federal district judge to seal the courtroom at the forthcoming trial of a former Goldman computer programmer accused of stealing the firm's computer code. The trial is set to start to late November.

http://tinyurl.com/25b8f3p

Indeed.

ReplyDeleteBecause President Barack Obama and the leaders of both political parties are unwilling to address the housing crisis and the wasting effects on the largest banks, there will be no growth and no net job creation in the U.S. for the next several years. And because the Obama White House is content to ignore the crisis facing millions of American homeowners, who are deep underwater and will eventually default on their loans, the efforts by the Fed to reflate the U.S. economy and particularly consumer spending will be futile. As Alan Meltzer noted to Tom Keene on Bloomberg Radio earlier this year: "This is not a monetary problem."

http://market-ticker.org/akcs-www?blog=Market-Ticker

Barach Obama: The Oligarch's President

ReplyDelete"When Barack Obama was elected, he had an unprecedented opportunity to shape American history by bringing the country's new financial oligarchy under control. Elected on a platform of change and renewal by a nation in crisis and with strong majorities in both houses of Congress, his election celebrated throughout the world, Obama could have done great things. Instead, he gave us more of the same. America will be paying for his decision for a very long time."

It is, in short, overwhelmingly clear that President Obama and his administration decided to side with the oligarchs -- or at least not to challenge them."

http://tinyurl.com/39plp5d

Very interesting hearing. But the most-interesting part of it is right here....

ReplyDeleteThe largest and most complex harm that may exist with the loans in default or foreclosure today is that the paperwork for the loans was not transferred correctly. I emphasize that what constitutes a correct transfer is a gray area; we need more direction from courts and legislatures on this subject. But there are plausible legal claims that the transfers of the notes and mortgages were not effective to give the trust full enforcement rights.

Uh, yep. That's the short version of where the problem lies.....

And it only gets better....

The implications of problems with transfer are serious. If the trust does not have the loan, homeowners may have been making payments to the wrong party. If the trust does not have the note or mortgage, it may not have standing to foreclose or legal authority to negotiate a loan modification. To the extent that these transfers are being completed retroactively, it raises issues about honesty in creating and dating the assignments/transfers and about what parties can do, if anything, if an entity in the securitization chain, such as Lehman Brothers or New Century, is no longer in existence. Moreover, retroactive transfers may violate the terms of the trust, which often prohibit the addition of new assets, or may cause the trust to lose its REMIC status, a favorable treatment under the Internal Revenue Code. Chain of title problems have the potential to expose the banks to investor lawsuits and to hinder their legal authority to foreclose or even to do loss mitigation.

http://market-ticker.org/akcs-www?singlepost=2233789

I guess our problems are their funding source?

ReplyDeleteThis Appears To Be Worthy of JAIL - RIGHT NOW

Worse: Two days before the loan was closed, the DNC apparently changed its privacy policy - it appears they may have effectively pledged their donor and contact lists without the consent of most of the people on them!

The DNC loan agreement as posted online by the Federal Election Commission (FEC) and signed by former Virginia Governor Tim Kaine (D) on September 16, 2010, says the loan collateral included: “All electronic mail (‘E-mail’) addresses and other contact lists, records and other Information (electronic or otherwise) relating to contributors, supporters and subscribers owned by any of the Borrowers.” The borrowers in this case were the DNC and the DNC Services Corporation.

The loan agreement further stipulates that if the Democrats defaulted, Bank of America would be entitled to “proceeds from any fundraising activity, refunds, reimbursements, or proceeds from the rental or sale of mailing, contact or subscription lists or Information (electronic or otherwise).”

WHAT?!

More to the point, are those lists worth anywhere near the amount of these loans?

http://market-ticker.org/akcs-www?singlepost=2233926

Make sure the banks get their bonus $...the country's priorities are upside down..........

ReplyDeleteInd. parents told drop disabled kids at shelters

INDIANAPOLIS — Indiana's budget crunch has become so severe that some state workers have suggested leaving severely disabled people at homeless shelters if they can't be cared for at home, parents and advocates said.

They said workers at Indiana's Bureau of Developmental Disabilities Services have told parents that's one option they have when families can no longer care for children at home and haven't received Medicaid waivers that pay for services that support disabled people living independently.

Marcus Barlow, a spokesman for the Family and Social Services Administration, the umbrella agency that includes the bureau, said suggesting homeless shelters is not the agency's policy and workers who did so would be disciplined.

http://www.palmbeachpost.com/news/nation/ind-parents-told-drop-disabled-kids-at-shelters-1001026.html

MUST SEE - Dylan Ratigan Interviews TARP Inspector Neil Barofsky - What The Fed Doesn't Want You To See »

ReplyDeletehttp://dailybail.com/home/must-see-dylan-ratigan-interviews-tarp-inspector-neil-barofs.html

H. R. 4646 - Cited As The "Debt Free America Act"

ReplyDeleteJust think, if you deposit $5,000.00 into your checking account or savings account the bank has to take out 1% or $50.00 of that money and send it to Washington . Then, any checks or cash you take out of your bank they will deduct 1% from what is still in the bank and send it to Washington . Total put in the Bank $5,000.00. $100.00 of that you give to Washington .

This bill, spells it out that everyone will pay the Government 1% of their gross income.

http://edegrootinsights.blogspot.com/2010/10/h-r-4646-cite-as-debt-free-america-act.html

All we get are lies...

ReplyDeleteThursday, October 28, 2010

Obama No Longer Bothering to Lie Credibly: Claims Financial Crisis Cost Less Than S&L Crisis

I’m so offended by the latest Obama canard, that the financial crisis of 2007-2008 cost less than 1% of GDP, that I barely know where to begin. Not only does this Administration lie on a routine basis, it doesn’t even bother to tell credible lies. .And this one came directly from the top, not via minions. It’s not that this misrepresentation is earth-shaking, but that it epitomizes why the Obama Administration is well on its way to being an abject failure.

The reason Obama can claim such phony figures is that many of the costs of saving the financial system are hidden, the biggest being the ongoing transfer from savers to banks of negative real interest rates, which is a covert way to rebuild bank equity.

http://tinyurl.com/2u7um37

Stiglitz: TARP Returns a "Drop in the Bucket" Compared to Damage Done

"The fact some of the banks paid back what was given to them on very favorable terms...is just a drop in the bucket compared to damage done to the economy," Stiglitz says in the accompanying video, taped at The Economist's Buttonwood Gathering.

Including the "enormous hidden subsidies to the banking system," the real economic cost of the bailouts is in the trillions, Stiglitz says.

"If the U.S. government had provided money to ordinary business at zero interest rates, what would our economy be like?," Stiglitz wonders. "What we did is give zero rates to banks, they then lent at much higher interest rates; that's the recapitalization. That's the gift."

http://tinyurl.com/29voxzh

No Mr. President, Larry Summers Did Not Resolve the Financial Crisis for a Pittance, He Just Papered Over the Problem

ReplyDeletehttp://www.huffingtonpost.com/william-k-black/no-mr-president-larry-sum_b_775307.html

A nation of sheep will beget a government of wolves" … Edward R. Murrow.

ReplyDeleteUntangling The Complex Foreclosure Mess

ReplyDeleteGretchen Morgenson has a fantastic interview and article over at NPR.

http://fedupusa.org/2010/10/28/untangling-the-complex-foreclosure-mess/

The States Take On Foreclosures

ReplyDeleteThe Treasury Department and the Federal Reserve have made it clear that they are more concerned about keeping the foreclosure mill going full speed than they are about determining whether the banks broke the law. Somehow throwing people out of their homes quickly is supposed to help the economy. Or so they keep telling us.

During the subprime bubble, homeowners who felt victimized by a mortgage originator or a bank could walk in the door of the attorney general’s office. Often, that’s exactly what they did. Employees in the A.G. offices looked at homeowners’ documents and interviewed them face-to-face — giving them a first-hand understanding of how bad things were. By contrast, the Office of the Comptroller of the Currency set up an 800 number in Houston for aggrieved consumers.

Not that the O.C.C. ever really worried about the exploitation of consumers. On the contrary, the O.C.C. and the Office of Thrift Supervision, the two primary federal regulators of the banking industry, viewed their role, incredibly, as protecting banks from consumers rather than the other way around.

Not surprisingly, the prospect of an alliance between Ms. Warren’s new bureau and a handful of activist attorneys general gives the banking industry the heebie-jeebies. At a panel at the Chamber of Commerce this week, Andrew Pincus, a lawyer with Mayer Brown, articulated their voluminous concerns.

http://www.nytimes.com/2010/10/30/business/30nocera.html?pagewanted=1&ref=business

Saturday, October 30, 2010

ReplyDeleteJP Morgan Chase Plays Fast and Dirty in Florida Loan Mod Waiver

Now here’s the sneaky bit. JP Morgan Chase never bothers to say that it regards filing that motion and going to the trouble of attending a hearing is just too much cost and bother to stop foreclosure action when it has started loan mod negotiations. And to add insult to injury, its sneaky wording makes it sound as if it lacks the power to halt the foreclosure process, as opposed to incur more costs (boldface ours):

Because Chase, as a plaintiff or servicer of your loan, is no longer able to unilaterally cancel a judicial sale in many Courts in the State of Florida….

This document is consistent with complaints we reported on earlier from Florida’s rocket docket, that foreclosures were finalized even when borrowers protested to the court that they were in loan modification programs. This is yet another example of how the banks are gaming the latest loan modification program, HAMP. Servicers collect fees for foreclosures and have the opportunity to apply the proceeds to the principal and interest advances they have made to investors. Those incentive far outweigh the puny fees the Treasury pays them to mod, but hey, if they can have both and placate Treasury by going through the motions of doing loan mods, why not?

http://www.nakedcapitalism.com/2010/10/chase-plays-fast-and-dirty-in-florida-loan-mod-waiver.html

Debt Collectors Accused Of Fake Courtroom, Judge

ReplyDeletePa. Attorney General Sues Unicredit In Erie

http://www.thepittsburghchannel.com/r/25569199/detail.html

No ones going to do it for you....get involved!

ReplyDeleteIts happening all over.........

Sunday, October 31, 2010

“Protest works. Just look at the proof”

It’s astonishing to see how Americans have been conditioned to think that political action and engagement is futile. I’m old enough to have witnessed the reverse, how activism in the 1960s produced significant advances in civil rights blacks and women, and eventually led the US to exit the Vietnam War.

In my column last week, I mentioned in passing something remarkable and almost unnoticed. For years now, Vodafone has been refusing to pay billions of pounds of taxes to the British people that are outstanding….

Many people emailed me saying they were outraged that while they pay their fair share for running the country, Vodafone doesn’t pay theirs. One of them named Thom Costello decided he wanted to organize a protest, so he appealed on Twitter – and this Wednesday seventy enraged citizens shut down the flagship Vodafone store on Oxford Street in protest. “Vodafone won’t pay as they go,” said one banner. “Make Vodafone pay, not the poor,” said another.

http://tinyurl.com/2wplb55

Sunday, October 31, 2010

ReplyDelete[Videos] 60 Minutes: (a) Anger in the Heartland (b) Deficits: Taxing the Rich

Two years ago, most Americans voted for change, and if the polls are to be believed, they're about to do it again.

In the latest CBS News/New York Times Poll, 80 percent said they want most incumbents out of Congress regardless of whether that incumbent is a Democrat or Republican.

There's a grim mood among people who were counting on a recovery that has now fallen flat. The economists who decide such things say that the Great Recession ended in June 2009. But since then, we've lost another half million jobs - which helps explain why there is so much anger in the land.

We saw a lot of it right in the middle of the country, among the people who've endured the recession longer than anyone.

http://tinyurl.com/3ans23x

Even before some of the nation's biggest mortgage lenders were forced to suspend foreclosure proceedings because of faulty paperwork, it was becoming clear that the Obama administration's year-old effort to pump life into the housing market was falling short.

ReplyDeleteIt wasn't "falling short." It was intentionally designed to produce lots of pretty colored candy in the form of "Hopium" but never actual results. HAMP and its pals never came with any sort of teeth in the form of actual punishment for non-compliance by the financial industry, and thus we have seen lots of things like this:

*

Homeowners being told not to pay - on purpose - so as to "qualify" for help. They are then denied a modification.

*

Homeowners who are put on trial plans but then send documents two, three, four or more times - with certified mail return receipts - and their servicers claim they "lost" them. Never mind that the homeowner has signature proof they were delivered. There is then no legal enforcement of that receipt - even though under virtually every form of legal agreement known to man a return receipt is proof of notice being received.

*

Homeowners who are strung along for months on "trials" and then denied a permanent modification. When the denial is rendered the entirety of the difference between the original payment and the trial is immediately due and payable, plus late fees and penalties for not making the original payments! This happens even though the homeowner is paying as directed on the trial modification.

*

Homeowners who are foreclosed on while on trials that allegedly are intended to "save their homes."

If true modifications - that is, real help - were the point of this entire exercise, rather than jerking people off and milking them for even more money when they can't pay, these actions would have exposed the servicers involved to severe financial penalties.

http://market-ticker.org/akcs-www?singlepost=2239509

ReplyDeleteWell that did not really help anyone...and he wonders why he gets booed at rallys...its because your a sell out!

ReplyDeleteMost health plans won't change much in 2011 — but costs likely will

If you were expecting dramatic changes in your workplace's health plan next year because of the health-care overhaul, here's some good news: Most employers aren't substantially changing their plans.

Now, here's the bad news: Employees' health-care premiums are expected to jump 12.4 percent, on average, in 2011. And if you work for a small employer, you'll probably pay even more, experts say.

http://www.sun-sentinel.com/health/os-open-enrollment-20101027,0,2870956.story

"Where's The Note" Update

ReplyDeleteSEIU or not, here is a status update from Where's The Note, as the recently launched campaign to request proof of mortgage note existence approaches the 20 day limit by law within which banks have to respond to all properly-submitted verification claims.

Heard Anything?

http://tinyurl.com/29neuda

Interesting post from someone at SEIU:

ReplyDeleteWe, like all of you, have been trying to bring attention to the chicanery that's been going down on Wall Street for years. Especially when it comes to banks using peoples' homes as chips in risky and possibly fraudulent bets. When the media started to catch wind about the robosigner nonsense, we scrambled to put the finishing touches on the site and go live. The result was about 100,000 visits to the site in the first three days. The very first responses from the banks were sort of haphazard and breathless - ie, they told the truth ("we have no idea where your note is"). But, they quickly circled the wagons and started replying with very standardized responses. Bank of America's response (and they're not the only ones) was the most shocking to us: "you have no legal right to see your note."

But, in all the responses, the vast majority of homeowners did not get their signed mortgage note sent to them as required under RESPA.

So far nothing here that loyal zero hedge readers wouldn't have guessed would happen. But, where do we go from here? It seems to me that the challenge before us is not trying to find potential fraud in the mortgage market. It will be picking which of the many, many blatant examples of potential fraud we want to pursue and drilling down on them. We decided, though, that no matter which avenue we take, the first thing to do out of the gate is to get these cases logged with state attorneys general. We have seen through media reports that banks are trying to use spin to put finite caps on the scope of the problems they've created in the mortgage market. Only 23 states. Just a few thousand homes. Mere procedural issues. Isolated incidents.

http://www.zerohedge.com/article/wheres-note-update#comment-692018

Lawmaker Questions Power to Foreclose .

ReplyDeleteA Virginia lawmaker asked the state's attorney general to launch an investigation of Mortgage Electronic Registration Systems, the middleman firm in millions of court filings that helps keep the mortgage-securitization machine moving.

Robert G. Marshall, a Republican member of the Virginia House of Delegates, requested that Virginia Attorney General Ken Cuccinelli determine whether the Reston, Va., company violates state law because it doesn't pay a fee every time a loan changes hands. Opinions differ as to whether MERS must pay local fees every time it sells an interest in a loan.

"There are too many people getting foreclosed on not properly," said Mr. Marshall, who represents two counties near Washington, adding that he is drafting a Virginia law that would require lenders to pay county fees before being allowed to proceed with foreclosures. "The disdain with which the conditions of law have been treated by those who want to make money too fast is very troubling to me."

Christopher L. Peterson, a law professor at the University of Utah who has criticized the record-keeping company's business model in scholarly articles, says the foreclosure furor is a serious challenge to MERS because the documentation problems show the company is doing an end run around hundreds of years of American property law.

"By having all the mortgage loans recorded in the name of one entity, the records don't mean anything anymore," Mr. Peterson said. "We used to have the records that showed the true economic interest of who owns the land in the public system. Now we just have one proxy, and we can't tell which lender or which trust owns the right to foreclose, because virtually every securitized loan is recorded in the name of MERS."

http://online.wsj.com/article/SB10001424052748704865104575588791583567372.html?mod=WSJ_hp_LEFTWhatsNewsCollection

Did you create this program to feed people to the wolves?

ReplyDeleteMortgage Modification Failures Push Borrowers Into Foreclosure

ray’s experience, in which homeowners get evicted while participating in programs designed to avert foreclosures, is being repeated thousands of times at the biggest mortgage firms, according to groups that aid borrowers. The government’s Home Affordable Modification Program came under fire at hearings last week for “trial” arrangements that allow late fees and debts to stack up and documents to disappear, triggering seizures.

“Many homeowners end up facing foreclosure solely on the basis of the arrears accumulated during a trial modification,” said Julia Gordon, senior policy counsel at the Center for Responsible Lending, in Oct. 27 Congressional testimony. “One incomplete payment or one accounting mistake can land you on an apparently unstoppable conveyor belt to eviction.”

http://www.bloomberg.com/news/2010-11-02/mortgage-modifications-meant-to-save-u-s-homes-push-them-into-foreclosure.html

from itulip:

ReplyDeleteThe Dem-o-crats are getting K I L L E D !

http://www.dailymail.co.uk/news/arti...ash-looms.html

http://www.dailymail.co.uk/news/article-1325782/Mid-term-elections-2010--Black-Tuesday-Obama-historic-backlash-looms.html

You climbed into bed with Wall St. WTF did you expect "Barry"?

I wouldn't be shocked in "Barry" threw his hand in & left Joe B to take over.

Bill Black Strikes Again: Fraud Of America

ReplyDeleteIt's a rather serious problem if you take a bite of one.

This problem is typically ignored -- at least by the financial sector and the mainstream media -- so we did "illuminate" the problem and the cause of action borrowers could bring for "fraud in the inducement."

We showed that the fraudulent senior officers that controlled home mortgage lenders created "liars," and NINJA loan programs designed to induce millions of Americans to take out loans they could not afford to repay. The endemic underlying fraud in the origination and sale of nonprime loans is critical to understanding why loan defaults are massive, why borrowers were typically the victims of the fraud and lost their meager savings due to the frauds, why loan modifications typically fail, and why foreclosure fraud has been so common. The endemic fraud also hyper-inflated the bubble and helped cause the economic crisis and severe loss of employment. Over a million Bank of America borrowers face these "challenges" that we "illuminated."

Yep. That's the issue, in a nutshell. Bill Black has been on this tirelessly, as have a few others, myself included. The mainstream media won't talk about it. I wonder why? Have you been watching CNBS and other "financial" channels lately? Notice who runs advertising on those networks? Uh, yeah.

http://market-ticker.org/akcs-www?singlepost=2248726

Here Is a Reason Why Mortgage Modifications May Be Moving So Slowly, The Servicer Gets the Vig!

ReplyDeleteFrom an astute BoomBustBlogger that reads the fine print buried in the middle of a 250 page servicer agreement…

IF THIS IS A TYPICAL PSA, NO WONDER SO FEW LOAN MODS BECOME PERMANENT. THE SERVICER GETS 25% OF THE FORECLOSURE PROCEEDS.

http://www.secinfo.com/d1Ax6e.u1u.c.htm

http://tinyurl.com/27ubofs

WSJ ARTICLE Foreclosure Crisis, Part 2: Modifications

ReplyDelete(((Ms. Risotto is full of it..there is no recourse..there is no follow through...been with Aurora..made all payments..transferred to IBM LBPS..now no record of paperwork)))SCAM

Treasury officials don't keep track of how many of the disputed loans are subsequently averted from foreclosure. Ms. Risotto says borrowers can call a counseling hotline if they believe they were wrongly denied.

((Mr. Barofsky hits nail on head)) Please look into Aurora Loan Services...scam city)

Mr. Barofsky says the oversight is toothless, noting that no servicers have been fined for bungled paperwork or improper foreclosures. At the request of nine U.S. senators, Mr. Barofsky is auditing whether servicers in HAMP are correctly following Treasury's guidelines when deciding whether borrowers should get a loan modification. The inspector general also is scrutinizing how borrowers are notified that they failed to qualify.

http://tinyurl.com/25bwuar

Geithner sold you out Obama...that or your collecting payment in India........

ReplyDeleteLet's Set the Record Straight on Bank of America, Part 2: Eliminating Foreclosure Fraud

Meanwhile, Bank of America expects to receive billions of dollars for its participation in HAMP. The top three banks (JPMorgan Chase and Wells Fargo being the others) will share $17 billion because HAMP pays servicers, investors and lenders for restructuring. These top 3 banks service $5.4 trillion in mortgages, or half of all outstanding home mortgage loans. Yet, as Phyllis Caldwell, Treasury's housing rescue chief has testified, there is no proof that these banks have any legal title to the loans they are modifying and foreclosing. In Bank of America representative Rebecca Mairone's response to us, she does not respond to, let alone contest, the fact that her bank, as well as other banks, has been illegally foreclosing on properties -- illegally removing people from their homes. Instead, she lists characteristics of those homeowners on which Bank of America might be illegally foreclosing: they are unemployed, they have not made payments in many months, a third no longer occupy their homes, and so on. It is interesting that she completely ignores all the important issues at hand with respect to the "deadbeat" homeowners. How many of these homeowners were illegally removed from their homes so that they became vacant?

http://www.huffingtonpost.com/william-k-black/post_1214_b_779193.html?just_reloaded=1

The episode of Jesse Ventura's "Conspiracy Theory" program on the TruTV network that was broadcast Friday and featured GATA Chairman Bill Murphy has been posted in three parts at YouTube. U.S. Rep. Ron Paul, the Fed's most informed critic in Congress, also has a big part in the program.

ReplyDeletehttp://gata.org/node/9267

Look at this...keep funneling money to bankers and sit back and watch this?...oh that's right your on a mission to India...can they understand people that talk out of two sides of their mouths?

ReplyDeleteYou've got to be one of the weakest Presidents ever!

Idaho officials poised to cut $8 million in Medicaid services to mentally ill and disabled

The agency has drafted a new set of rules that authorize cuts in services or elimination of some programs designed to trim about $1.6 million from its current fiscal year budget. Those cuts, however, would also trigger the loss of another $6.5 million in federal Medicaid matching funds used to reimburse care providers.

http://www.canadianbusiness.com/markets/market_news/article.jsp?content=D9J4MBBO0

What recourse do homeowners have when servicers fail to comply with the program? So far none and Tim Geithner really could care less...

ReplyDeleteTreasury Department Says HAMP Doesn't Put People Into Default

Alan White, a professor at Valparaiso University law school, pointed out that a common complaint from HAMP applicants is that their servicers tell them they can't get help until they fall behind on payments. According to the Making Home Affordable call center report from February (PDF), 10.9 percent of all HAMP complaints arose from servicers telling borrowers they must be delinquent to be eligible for help. It's the fourth-most common HAMP gripe.

"Treasury is just wrong," said White. "I really wish Treasury would stop defending the banks and start acknowledging that they are preventing HAMP from achieving its goals."

http://www.huffingtonpost.com/2010/10/26/treasury-department-hamp-_n_774249.html

IBM loan services -Big Blue and Big Banks get together

ReplyDeletehttp://ibm-lender.pissedconsumer.com/ibm-loan-services-big-blue-and-big-banks-get-together-20101107206099.html

Principles for sale??????....how apropos

ReplyDeleteJanet Tavakoli on Bank & Foreclosure Fraud

Janet Tavakoli, Tavakoli Structured finance, and I discuss bank and forclosure fraud via Goldman Sachs, JP Morgan, Countrywide, Bank of America, Citigroup etc. in the video commentary above.

http://tinyurl.com/349ykyf